Does IFRS apply to management accounting? What management accounting methods are taken from IFRS? What methods are contrary to IFRS, but are used for internal purposes?

PwC Academy’s experts will share interesting practical examples on this topic.

We usually starts our training courses on finance with a discussion of IFRS applicability for management accounting purposes. The argument in favour of harmonizing two accounting systems (financial and management) is to avoid unnecessary discrepancies in income that need to be explained to management. It is a kind of 'lean' accounting that saves finance department resources for reconciliation. However, there are management accounting methods that are fundamentally contrary to the IFRS principles, though they are useful for obtaining a new look at the business.

Example #1. Different approaches to cost classification

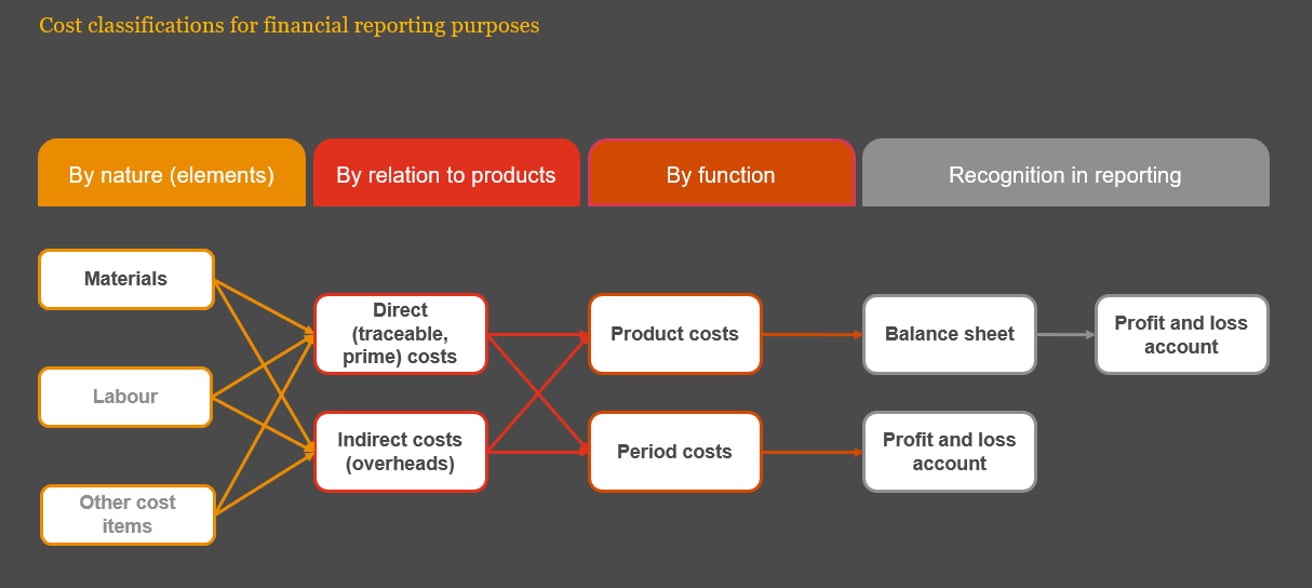

Accounting standards provide for three main ways to classify costs (Figure 1):

- By nature. IAS 1 “Presentation of Financial Statements”, para 102. An entity aggregates expenses within profit or loss according to their nature. For example, material, labour or expense cost.

- By relation to product. IAS 2 “Inventories”, para 12-13. Based on the relationship or degree of traceability to products, the costs are classified into direct costs and indirect costs (overheads). This is important for determining the cost per unit and then tracking this value until the moment the product leaves the balance sheet (sale, write-off).

- By function. IAS 1 “Presentation of Financial Statements”, para 103. The cost can also be classified by the business functions for which the resources have been used. For example, cost of sales, distribution or administrative costs, or in other words production (product costs) and non-production costs (period costs). This cost breakdown is dictated by the main goal of financial accounting, that is to determine what are assets (balance sheet) and what are expenses (profit and loss account). Those whose KPIs depend on profitability and turnover ratios understand.

Figure 1. Cost classification for financial reporting purposes

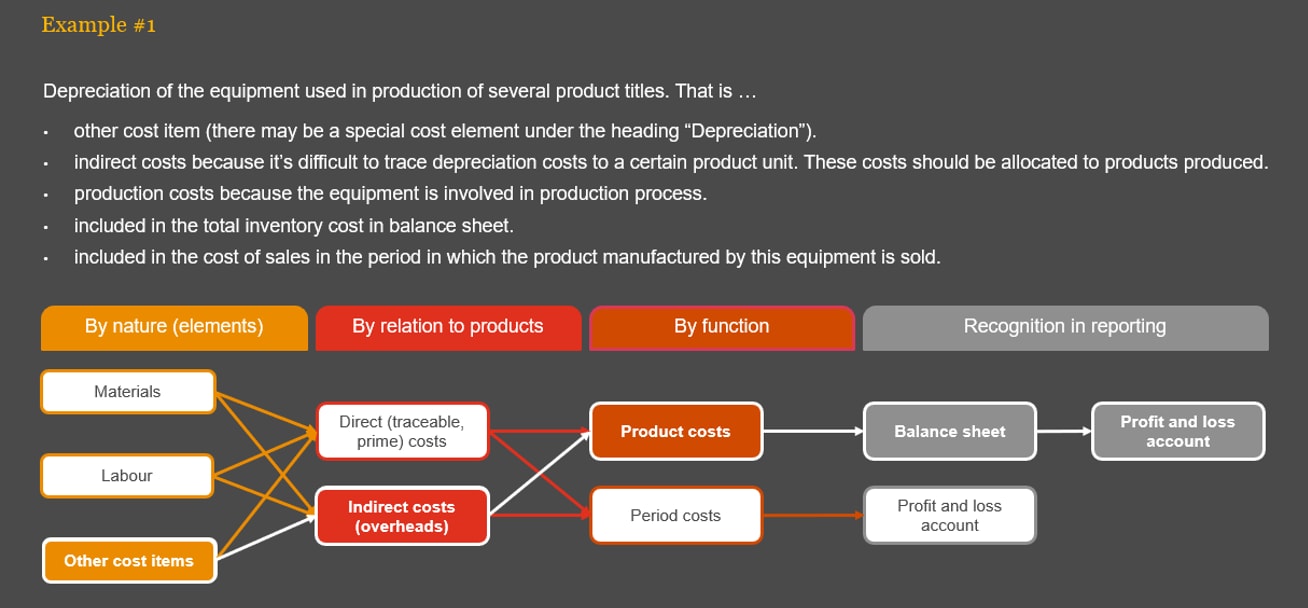

Figure 2. Example of cost classification in financial reporting

The classifications described above can also be found in management reporting. However, management accounting has its ‘own’ cost breakdowns which are not mentioned in IFRS:

- For planning purposes we typically classify costs by their behaviour: fixed, variable, semi-variable, step costs, etc. Cost behaviour is the way in which costs are affected by fluctuations in the level of activity (for example, number of units produced, number of labour hours, etc.). Are we interested in knowing the share of fixed costs in the product cost of our competitors? Definitely yes. If the demand in the market and the production output change, then it is possible to predict how costs will change, and possibly prices for customers. In stagnating markets, firms with lower fixed costs win, as variable costs can be avoided during output cuts. It is important for an investor to pick up such firms just before the recession begins. Information about fixed and variable costs has commercial value. Public disclosure of such data makes a company ‘naked’ to the competition, that’s why the company keeps the information in secret.

- For controlling and performance valuation purposes: controllable and non-controllable costs.

- For decision-making purposes: relevant and non-relevant costs.

Outcomes:

#1. IFRS is a good methodology because it has been proven by experience, but not everything needs to be accounted in compliance with IFRS. For the sake of success in business, it is possible and even necessary to deviate from IFRS, but only in management accounting.

#2. It is important that the finance function listens to its internal clients (business line managers) and understands the real reasons for calculating costs. The essence of the business task determines the choice of cost breakdown. If the problem is not understood correctly, then either the business line manager will get useless information, or the financial manager will have to stay at work and redo his/her analysis. In both cases, the company loses time to make the right decision.

Contact us