However, supply chains remain highly vulnerable to social and environmental issues, due to several factors, chief among them:

The lack of visibility into all tier suppliers.

Complex interpretation of requirements

Internal and external data dependencies

And emerging unforeseen supply chain risks

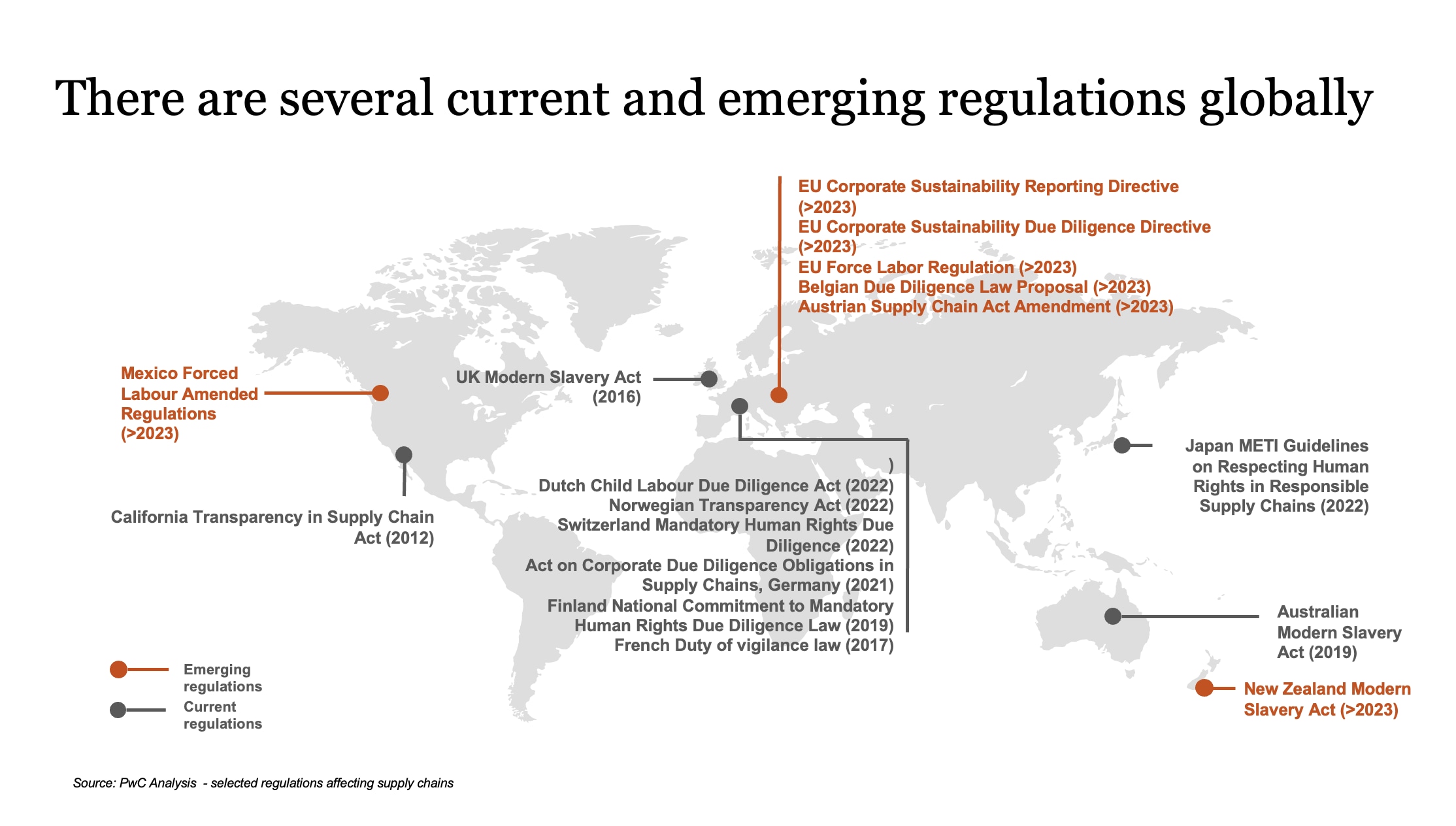

Regulatory landscape - new obligations entering the arena

The past months were an opportunity to observe both the EU and selected member states trying to address these key challenges by adopting new due diligence rules limiting environmental and labor risks in corporate supply chains. The United Kingdom, France, the Netherlands, Norway, and Austria are among the countries that already have modern slavery or human rights due diligence laws in place. Germany, by introducing its Supply Chain Act, also aims to drive corporate sustainability in global value chains, advance the green transition, and protect human rights.

And more is coming with an important milestone that was the 1st of June, which put supply chain management and its challenges firmly front and center. Members of the European Parliament delivered their final position on the EU’s corporate sustainability due diligence directive (CSDDD). The development of this Directive represents a momentous opportunity to ensure that companies conduct meaningful human rights and environmental due diligence throughout their value chains. But the content of the duty matters just as much as its existence. It’s key to align the obligations as closely as possible with the existing, international standards for sustainability due diligence – the UN Guiding Principles on Business and Human Rights (UNGPs) and the OECD Guidelines for Multinational Enterprises. The new regulation will only apply to certain companies headquartered or operating in the EU, however, their business partners and other companies in their value chains in key sourcing and production markets outside the EU will also be affected.

What key challenges organizations and investors should be aware of?

Supply chains can be highly complex. They often span many countries and include multiple tiers, which are made more opaque by outsourcing and offshoring. They are also essential to the success of almost all businesses and can be a significant source of value creation and innovation. As supply chains fall outside of a company’s core operations, they expose them to hidden and uncontrollable risks typically driven by ESG factors, such as natural resource depletion, human rights abuses and corruption.

These issues can harm the reputations, operations and financial performance of businesses or assets owned by investors, as well as investors’ own reputations and investment performance. Compliance with local regulation is rarely sufficient to meet stakeholder expectations (certain countries in which a supplier may operate may have less robust legal and regulatory standards than others).

While a company may implement the highest ESG performance standards in its own operations, many of its suppliers may not hold similar practices. Studies have estimated that up to 90% of a company’s sustainability impacts originate in a firm’s supply chain. These impacts can hold considerable risk: notably, companies such as Nike, Marks & Spencer, and Hershey’s experienced firsthand the reputational and financial fallout caused by ESG-related issues in their supply chains.

What does a supplier ESG profile include?

Environmental

refers to the resources a supplier uses, the waste it produces, and the resulting consequences of those activities on the planet. This includes water management, greenhouse gas (GHG) emissions, and the use of dangerous chemicals.

Social

refers to how a supplier manages its relationship with internal and external stakeholders. This includes labour relations, employee training and education, reputational issues, and how a supplier fosters positive relationships within the broader community.

Governance

refers to a supplier’s internal framework of procedures, practices, and controls. This includes internal processes utilized to govern itself, comply with regulations, conduct external audits, and guide decision-making.

What key steps can companies take to shore up their supply chains?

ESG performance is increasingly considered a component of resilience. Companies with strong ESG performance often have robust governance frameworks, manage social and environmental risks well, and have stronger relationships with suppliers. Weak ESG performance, on the other hand, can carry significant reputational and operational risks for a company. Prioritizing supply chain sustainability can, therefore, reduce general risks by minimizing operational disruptions due to environmental risks, regulatory risks, or reducing reputational risks caused by labor issues.

In order to do so you should increase your capacity to anticipate risks: plan for global scenarios and increase visibility across suppliers. Tools that quickly identify suppliers with higher or lower material ESG risks across your entire supply chain, like PwC’ Sustainable Value Chain Checker, can help increase visibility.

The two United Nations summits, the COP27 UN Climate Summit in November and the UN Biodiversity Conference, COP15 in December, covered many important areas, but clearly highlighted that governments are applying a global lens to the crises of climate change and biodiversity loss. As this approach feeds through to regulations, companies can expect to be held accountable for the environmental impact of their entire value chain.

While one can control what their own organization can achieve, it’s in the supply chain that the battle for climate, nature and other sustainability issues will go on. According to the Carbon Disclosure Project (CDP), greenhouse gas emissions in a company’s supply chain are, on average, 11.4 times higher than its operational emissions. When large corporations focus on the scope 3 emissions, many small and medium sized enterprises may find that they suddenly no longer comply with their buyers’ requirements.

A multifaceted approach is necessary to meet these challenges, centring on three areas: data, technology and collaboration. Large corporations can share knowledge and resources with smaller businesses. Governments, industry bodies and NGOs should all play their part through policy changes and industry standards. The EU recovery package, for instance, includes funds directed toward assisting green food supply chain strategies, green transport options, and circular economy initiatives.

Climate-smart supply chain planning will play a significant role in supply chain management in the upcoming years. Higher temperatures, extreme weather events, sea-level rise, and water shortages affect the availability of crucial materials and resources. That’s why it's so important to integrate environmental considerations into procurement decisions: set environmental benchmarks for potential suppliers and integrate ESG ratings into the procurement decisions. In addition, analyzing the existing suppliers’ environmental performance plays a key role in identifying high and low risk performers in terms of their environmental stewardship and call for performance improvement, when needed.

Social aspects have been moving up on the multinationals’ agenda in recent years. The European Union’s current efforts to introduce rules to hold companies accountable for social and environmental risks in their supply chains further accelerate that ascent.

There are already guidelines in place to address human rights breaches in the private sector. This year marks the 12th anniversary of the United Nations Guiding Principles on Business and Human Rights (UNGPs). The Guiding Principles provide a global framework and clarify the role of business enterprises, including investors, with respect to human rights. Under the UNGPs, companies are obliged to undertake human rights due diligence. The process is meant to ensure that potential adverse impacts stemming from companies’ activities in global operations, supply chains, and business relationships are identified, addressed, monitored, and remediated.

Even though there is no comprehensive survey on companies' respect for human rights, benchmarks and ratings that have emerged over the years indicate some progress and opportunity for improvement. According to the 2022 Corporate Human Rights Benchmark, a growing number of companies are taking up the UNGPs, with their commitments and procedures described as strong; still, too few companies manage their responsibility adequately. For example, almost 40 percent of all companies assessed in 2022 did not score any points under the due diligence indicators1.

Recent calls for protection of workers’ health and safety, decent working conditions and equal treatment have resulted in greater attention on the social performance of a company’s suppliers. Regardless of the procurers’ social performance, companies can face significant financial and reputational risks when their suppliers violate labour laws, discriminate, or negatively impact their local communities.

Companies committed to strong social performance across their supply chains mitigate these risks and benefit from positive publicity and brand differentiation. That’s why companies should communicate social performance expectations with suppliers including messaging from senior executives and implementing social performance requirements in procurement contracts.

The European Union released guidance in 2020 for corporations to implement effective human rights due diligence practices to address the risk of forced labor in their supply chains. Similarly, Germany has introduced its own supply chain due diligence legislation in 2023. The EU Taxonomy requires financial market participants and large companies in the EU and UK to publicly disclose their alignment with certain environmental objectives. Companies can expect to be under greater scrutiny by investors, consumers, and other companies for details on the material issues affecting their industry’s supply chains. With regulatory trends in supply chain disclosures expected to accelerate in the coming years, companies should begin to collect relevant data and be prepared to report on their upstream ESG performance. And this is where technology and innovation will play a key role.

Supply chain sustainability shifts the focus from short-term financial considerations to long-term value creation, and considering and managing the ESG performance of one’s suppliers. By including such considerations, sustainable supply chain management not only benefits the environment, but also reduces risks, mitigates impacts, and realizes reputational and financial benefits, such as cost savings, brand goodwill, and customer loyalty.

Skontaktuj się z nami

Ewelina Łukasik-Morawska